26 April 2026

How to beat the flatline business blues: why you should be buying assets

Flatlining in an agency is an exhaustive way to survive. In this article I make the case that almost any profitable agency can acquire to extend the growth stage of it's lifecycle. Next week... I look at building as opposed to buying.

It's surprising how many agency owners I speak to have had ‘the conversation’. Another agency knocks on the door and floats the idea of being acquired. The owner listens politely, says something noncommittal about timing or priorities, then goes back to client work. The approach gets filed under "interesting, but not for us" or "maybe one day", or worse still, "I wish".

I understand why. Running an agency is already a full contact sport, so why volunteer for a second job when the first one already has you on your knees? If you are on your knees, fighting fires, vanquishing volatility, then deflecting ‘the conversation’ is the right instinct. But… if not, I think the near-automatic deflection could be costing owners more than they realise, and in this article I'll explain why.

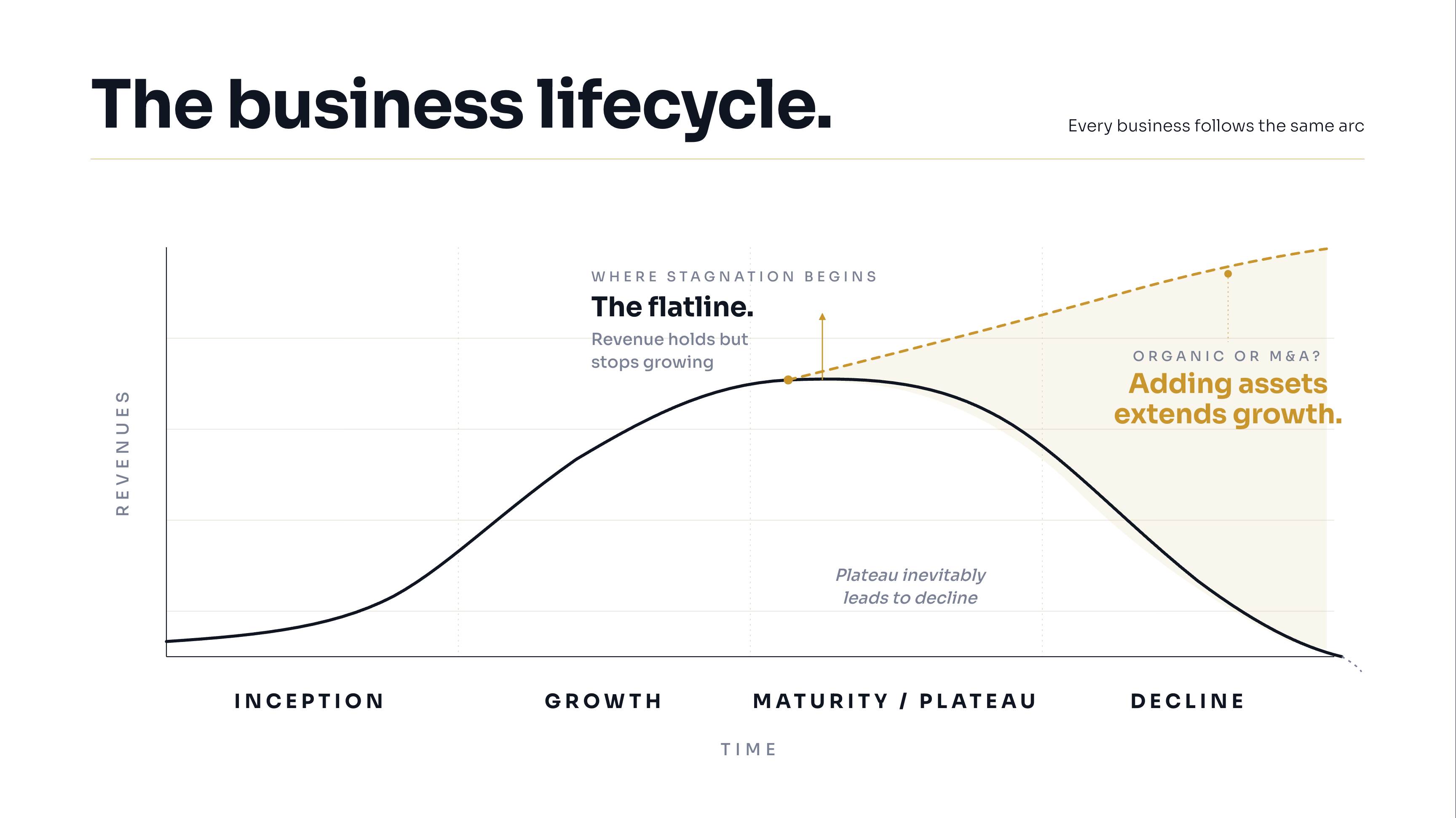

The plateau is coming for everyone

Every business sits somewhere in a lifecycle, from inception through growth to maturity and eventual decline. In agency terms, there's a period where new business comes in faster than you can staff it. It’s an amazing time to be in any agency. But then one day that stops. When it does the agency has reached maturity for the model that’s set up; the business is in plateau, neither growing nor shrinking. If it happens to you, unless you change your commercial model, extend your offering, move into a new vertical or geography, or build a genuinely new capability in-house, the plateau can last for years. Organic growth is wonderful when it's working, but it's painful when it stops.

But let’s call the plateau what it is. Stagnation.

Like sharks, agencies that stand still go into decline and eventually die. Stagnation inevitably leads to decline. How a stagnating agency lives is a function of how adept the leadership team is at managing client and people churn whilst juggling eroding margins. My observed truism is that stagnation leads to death in the same predictable way that income follows assets.

I’d like you to think about the second half of the above sentence for a moment. It hold the key to the way out. I’ll repeat it for emphasis: income follows assets.

If you want to extend the growth phase of your business, you have to keep adding assets to it. Assets come in many forms. Proprietary capability is one. IP, distinctive commercial models, and well-executed operating systems all count too. My own three systems approach to running an agency is itself an asset, because a business that runs on coherent systems is worth more than one that runs on Excel.

You can build these assets yourself, and sometimes that's exactly the right thing to do. Building gives you something you own, shaped to your business, and it doesn't require you to take on someone else's culture or commercial baggage.

The trade-off is time which is all of our most precious resource. It’s certainly mine as I head towards my sixtieth year at pace.

Building a new capability in-house can take years before it materially moves your revenue, and the stability of early plateau doesn't hang around while you ponder. Whereas, acquiring another business brings a new asset in within a calendar year. It compresses the timeline and that’s why I love it as a strategic option: it can be a fast route to beating the flatline blues. It can buy you reach, capability, and revenue at a pace internal investment can't match; it lets you bolt on a service line your existing clients already want; it widens the engine in a way that boosts next quarter's numbers rather than the one after next year's.

This article is about that route because it's the answer most owners reflexively dismiss when they have ‘the conversation’. Of course it’s not the only route to beating the blues, but it is a highly effective one. I know, I’ve done it.

My concern (and the reason for writing this blog) is that M&A’s dismissal by agency leaders is usually based on objections that need examining more carefully.

Acquisition is one of the few quick and credible answers when organic growth slows to a crawl. It buys you a future at a pace internal investment can't match. It's also the quickest way to turn an agency from a job you own into an asset that has its own value, independent of your daily presence.

That last point is the one you might want to think about when you wake up in the middle of the night.

If you've never thought of your agency as an asset, only as your work, then acquisitions feel like a distraction from the real thing. But, once you do think of your business as an asset, acquisitions become one of the obvious tools for making it more valuable.

The objections, in the order they usually appear

When I press owners on why they don't engage with the inbound approach, the objections come in a predictable order.

The first is "I'm not equipped." This is honest and probably true, but it's also the easiest to fix. M&A is a learnable discipline, not a dark art, and the gap between "I've never done one" and "I know how to evaluate one" is a few weeks of focused effort, not years.

The second is "it'll distract me from the core business." This is a real risk if you treat each deal as a bespoke project assembled from scratch, but it's a manageable one if you build a capability that lives somewhat separately from day-to-day delivery. Moreover, if you do think of your business as an asset that is run day-to-day by the team you’re paying well, building the asset becomes the job.

The third, and the one that is probably hardest to admit, but most common, is cash. Owners look at the price tags on agencies they'd consider buying and conclude they can't afford it. They mentally compare the purchase price to their own bank balance, find the gap unbridgeable, and stop thinking about it.

Is the objection really about cash?

Here's where it gets interesting. I find the cash objection often turns out to be a proxy for something else.

Sophisticated buyers rarely fund acquisitions out of their personal current account. Deals get structured with a mix of cash, seller financing, earn-outs tied to performance, and external capital. The price you see at the top of a heads of terms isn't the cash you need on day one; it's the headline number that gets delivered across several mechanisms, each of which spreads risk and timing differently. It’s called structuring. Understanding deal structuring was the biggest “aha moment” in my own M&A journey. It took me from seeing acquisition as something other people did to seeing it as inevitable for me. Understanding structuring shifts the frame from "do I have the money" to "is this deal worth doing on terms that don’t expose me to disproportionate risk."

Which is exactly when the deeper objection comes to the surface. Debt.

Many agency owners don't like the idea of using debt. They've built their business carefully, often without external funding, and the prospect of taking on borrowing to buy something else feels reckless.

I come across many owners who see debt as a bad thing, full stop, rather than as a regular tool that disciplined businesses use to grow. That view is, of course, perfectly reasonable. But it’s also what allows more sophisticated buyers to outcompete them. The cautious owner waits for the day they can write a cheque from cash; the sophisticated buyer structures a deal, uses sensible leverage, integrates well, and is on to the next one whilst the cautious owner is still saving up.

To be crystal clear, I'm not arguing that every owner should rush to take on debt. I am arguing that if your instinctive answer to "would you use borrowing to fund a good acquisition" is no, you're playing a different game from the people who keep buying the agencies you might have wanted.

One deal is a project; more than one is a capability

If you do decide that acquisitions are part of your growth strategy, the next mistake to avoid is treating the first one as a one-off. A single deal can absolutely work; people get lucky, or they have a great advisor, or the target turns out to be in better shape than expected. But I know loads of owners who’ve bought all or a part of another agency only to be disappointed. They bought because they could, or it looked like a great deal, but they didn’t really have a plan. Frankly, they didn’t really understand the single most important thing about buying assets. Buying isn’t the hard part, it’s what you do with it and where it fits into the long-term plan that matters. And, if you do have a plan and you can make it work, why only buy one? If it works, why stop?

Through my involvement with the Digital Agency Business community, I’m meeting a slew of super smart agency owners who see programmatic acquisitions as a central plank of their plan. They have committed time, energy and resource to building a repeatable capability that keeps them adding assets. Remember, income follows assets. Always.

A repeatable capability has four moving parts, each of which needs to exist before you start.

Dealhunting

You need origination, which is the unglamorous discipline of generating a steady flow of targets rather than waiting for inbound. The owners I see succeeding here treat sourcing the way good salespeople treat pipeline; they have a target universe, a regular outreach programme, and a tracking system that means they can have ten conversations open at once without losing the thread.

Diligence

You need the commercial pre-diligence knowhow to assess an asset before you involve lawyers and accountants. This is the work of reading the business honestly: the client concentration, the team's actual capability versus the marketing, the revenue quality, the cultural fit. It's the part you can't outsource, because it requires judgement about your own business as much as theirs, and it's where most bad deals get killed before they cost you serious money. I looked at 250 to buy 13.

LOI / Heads of Terms

You need an LOI / Heads of Terms process and a model that ties price to risk rather than to comparable transactions. Two deals at the same multiple can carry wildly different levels of exposure depending on how they're structured; the buyer who understands this protects downside while still being competitive on price.

Post-acquisition plan

You need an integration playbook. As I mentioned earlier, anyone can buy a business, it’s just big scale shopping. But when you buy a business, you won’t see any value from it unless you have a plan. Integrate everything or just the back office? Does the name stay above the door? What policies of your business will they need to adopt? How much freedom will the unit leaders have to make decisions? Are you moving banks? How are you going to hold onto the best people? How are you communicating with new clients? When?

The deal that looks great on the LOI is the deal that fails after close if integration is an afterthought. Day one, day thirty, day ninety; who owns what, which systems get unified, which clients get a personal call, which staff need reassurance.

The team structure that supports all this doesn't have to be enormous. A small internal acquisition function, working alongside external advisors who bring deal experience and specialist diligence, can run a serial acquisition strategy while the rest of the agency carries on serving clients. Remember, if you see serial acquisitions as part of your strategy, this is your job. Get your hands off the day-to-day tiller and trust your people to steer the ship.

The point is that the M&A playbook exists as a capability, not as a hectic side project the founder is trying to squeeze in between client meetings.

What to do with this if it's landed

If any of this has prompted a flicker of recognition, the first step is to increase your knowledge of the process, the mechanics, and the impact on your business model. It’s tempting to go and buy something, but I’d urge you to resist the temptation until you’ve done your homework.

There are several routes to capability. There are good books on M&A, particularly those written for owner-operators rather than corporate strategists. There are structured courses, including Peter Lang's, which is built specifically for agency owners. There are expert advisors who can walk you through the process; I do this work myself, so do get in touch if it would help. And there are bootcamps, which are the right answer if you want to compress the learning into a focused window with a small room of peers doing the same work.

I'm going to one of these next week, in fact. Peter is running his Boston M&A Bootcamp on the 30th of April and 1st of May at Convene One Boston Place. It's a small-room, action-first format covering pipeline, commercial pre-diligence, LOI structure, and post-close integration; the kind of work that's hard to learn from a book because it benefits from doing it in the room with other buyers. If you've been thinking about this and want to accelerate, you can find the details here. I'd be glad to compare notes if you're going.

If none of these appeal to you, do something that’s free. Sit down somewhere quiet, set every objection aside (ban the black hat) and answer one question as truthfully and openly as you can: if cash, capability and risk weren't issues, what would you buy to boost the value of your business this year?

If you have an answer, you've crossed a line. You've started thinking like an owner of an asset rather than the operator of a job. If you don't have an answer, it tells you something useful too; it means the next step isn't a deal, it’s probably going back to strategy 1.01 to remap your future.

Either way, the inbound approach next quarter deserves a more considered answer than the polite deflection. The plateau is patient, the buyers (your competitors) who've built the capability to keep growing through it are not.

Next week, I'm writing about building assets to extend the growth stage and I'll also file a report from Boston!

Dom Hawes

Dealhunter

Dom Hawes is an M&A adviser focused on creative and consulting businesses. After building and scaling a multi-agency marketing services group through acquisition, he now works full time on originating, structuring, and executing deals for founders and investors. He specialises in sub £20m revenue businesses, with particular expertise in buy-and-build strategy, deal sourcing, valuation, and transaction structuring. Dom writes about mergers and acquisitions, value creation, and the realities of building and exiting services firms.

Related reading

16 June 2026

Innovate? How the hell do we do that!

Innovation, the noun, freezes people; innovating, the verb, gets them moving. Ben Bensaou's Built to Innovate shows how agencies can turn that shift into a habit, building a second engine before AI forces the question.

1 June 2026

The Chasm Is Opening in the Agency Market. Which Side Are You On?

Market dislocations transfer assets from the operators who can't adapt to those who can. AI is doing it to agencies now. Revenues might still look healthy and maybe nothing feels like a crisis? Read on...

10 May 2026

What is a buyer thinking when I sell my agency?

Buyers don't buy to remunerate you for the past; they're buying your future. Numbers get you through the gate, but it's chemistry that decides the deal, often inside ten minutes. Prepare to be real, not perfect.